The Private Equity cycle is being stretched with longer holding periods

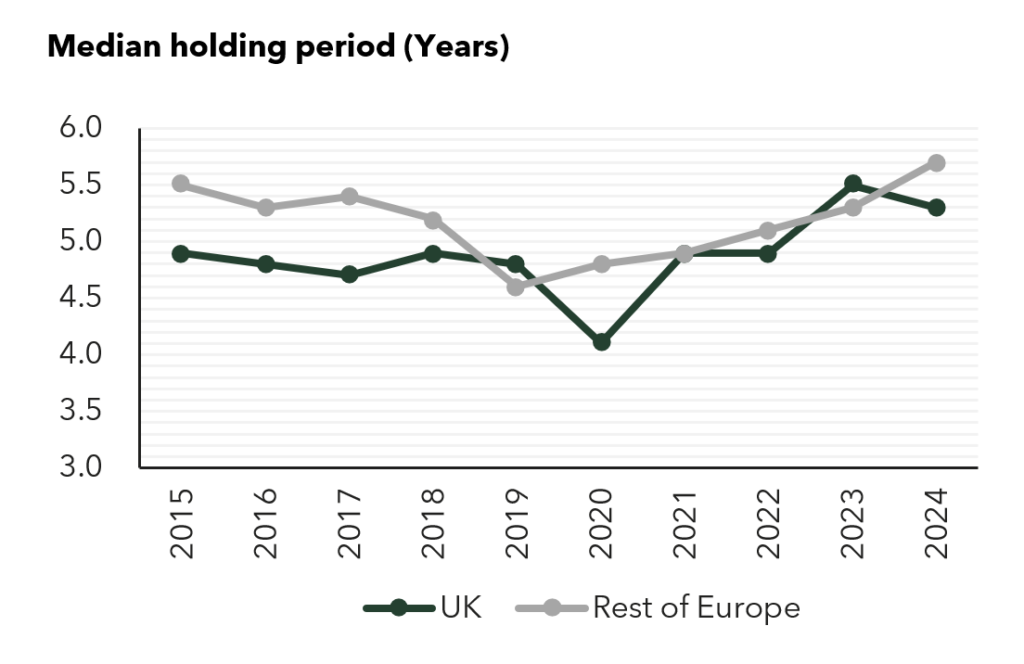

In the UK, holding periods for Private Equity firms have been near their 10-year high, with median ageing of Portfolio Companies that exited in 2024 at 5.3 years, up from 4.1 years in 2020.

This is part of a wider global trend that sees median holding periods of 5.8 years, driven upwards by data for the Rest of Europe and US & Canada.

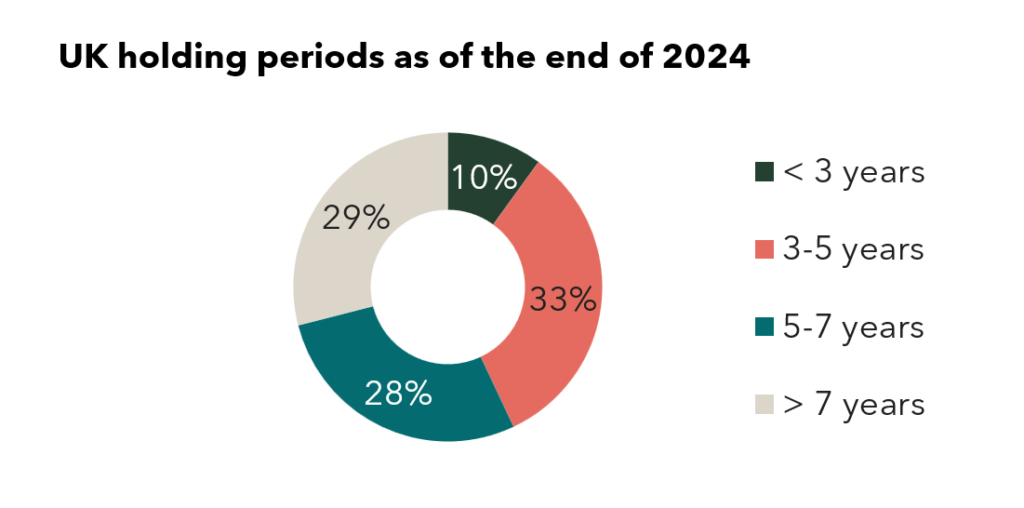

Among recent UK exits (2024), more than half (c.57%) had been held in the portfolio for over 5 years; and c.29% for over 7 years, as shown in the chart below.

The reasons behind the trend? They can be summarised by two schools of thought:

- Thesis #1: Difficult exit conditions.

- As reported by Bain & Co, the current adverse market environment has been the main impediment to exits and crystallising returns according to c.60% GPs and c.70% of LPs. Together with unfavourable and slow market for dealmaking, respondents also pointed out asset valuations (wider bid-ask gap), high interest rates andgeopolitical uncertainty among the biggest threats to exits.

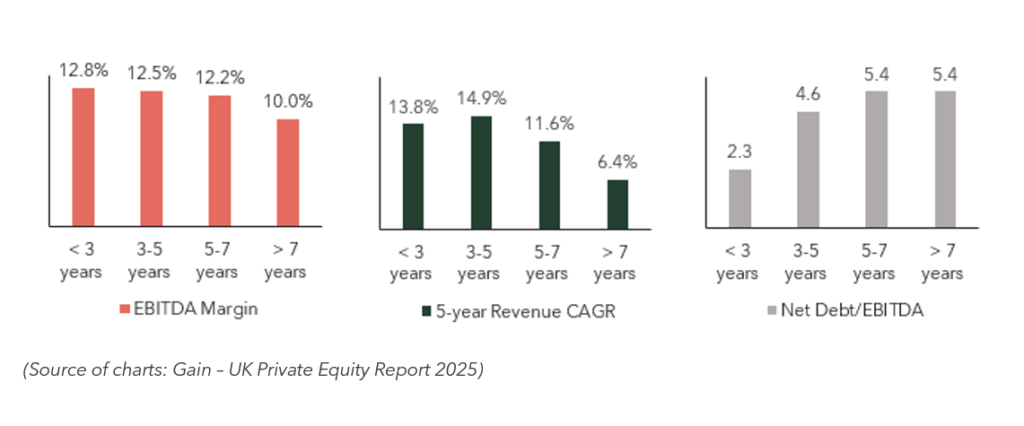

- Behind Thesis #1 there could also be underlying issues with Portfolio Companies: in fact, aged Portfolio Companies (over 7 years) tend to have lower margins and slower growth rates which contribute to them remaining unsold for longer – see charts below.

- Thesis #2: Desire to hold on to prized assets.

- An alternative interpretation sees longer holding periods as the sign that sponsors want to retain strong-performing assets for longer.

- They can do so by requesting a fund extension or rolling their investments into continuation vehicles.

- Note the ageing data above is measured as ‘no. of years since last deal’. As such, if sales to continuation funds are classified as an exit, this would artificially reduce holding periods reported.

Continuation funds are becoming more commonly used but they carry risks.

Against this backdrop, PE sponsors who face impending fund maturity have started using continuation funds to transfer one (or more) Portfolio Companies from an existing, maturing fund into a new vehicle. Such vehicle is typically managed by the same GP.

The appeal of continuation funds can be traced to the solutions and benefits they provide to the stakeholders involved, particularly:

- GPs defer an exit during a downturn and raise new funds to participate in the next phase of growth of a high-conviction asset, with a view to achieve higher returns in the future;

- LPs either cash out or roll over the position to the new structure; and

- New investors acquire stakes in mature assets, with shorter exposure.

As reported by the investment bank Jefferies, In H1 2025 continuation funds accounted for $41bn of GP-led deals. It is estimated that c.19% of sponsor-backed deals reaching the end of their term exit via continuation vehicles; LPs expect this figure to increase further to 29% by 2030.

However, issues with continuation funds are two-fold:

- 1. There are fears they can be used to hide underperforming assets: a McKinsey survey indicates c.30% of LPs consider assets in these vehicles as ‘distressed’ or ‘challenged’. If a PE house is struggling to sell a certain asset, then a continuation vehicle will not necessarily fix underlying issues, unless the new vehicle provides fresh capital and a revitalised strategy. As such, it is paramount to provide stakeholders with clarity around how the next phase in the lifecycle of the asset is going to be different.

“Aged assets can represent a value investment opportunity or even allow opportunistic buyers to consolidate several long-held investments. However, careful consideration should be given to the ultimate exit options for the acquirer. If the continuation vehicle was set up due to challenges delivering an exit, there is a risk that future buyer appetite might be lower and the asset could be perceived as ‘tarnished’ or ‘unloved'.” Richard Harrison, Head of Special Situations M&A, KR8 Advisory

- 2. Continuation funds are inherently prone to potential conflicts of interest among stakeholders, namely:

- GPs are sitting on both sell-side & buy-side: this might distort valuations by providing incentives to sell at a higher exit value to obtain larger carried interest;

- Old LPs are looking to maximise exit value; whilst

- New LPs want to minimise asset price and avoid overpaying;

- Management: are the senior team still committed to drive value for the new vehicle? There’s a risk it might not if the exit triggers the crystallisation of any ‘sweet equity’. Therefore, it may be important to reset the Management Incentive Plan.

The above issues highlight the need for transparency and alignment of incentives between GPs, LPs and Management teams. In part, comfort can be obtained by engaging advisers performing independent valuations and monitoring post-deal performance.

Conclusions: what this could mean for the private equity industry.

We appear to be witnessing a permanent shift in the traditional view that a PE cycle lasts 4-5 years. Continuation vehicles are being used to support new fundraising attempts without fixing the underlying challenges that might exist in aged portfolio assets.

Holding assets for longer or using continuation vehicles are perpetuating a self-reinforcing cycle: what started as a response to poor market conditions for exits is now getting in the way of new fundraising, thus creating a logjam in the PE cycle which further reduces overall deal volumes.

The trend could reverse once market conditions improve. However, we live in a world of perpetual volatility and uncertainty which will encourage longer term hold strategies for certain assets and the need for GP’s to be more creative regarding how they unlock value in trickier investments.

How can KR8 help?

As PE firms navigate a longer and more complex investment cycle, KR8 can bring clarity and decisive action, in the form of proactive investment management. We are supporting PE clients protecting value and unlocking growth with end-to-end lifecycle support:

- M&A Advisory: we provide clear buy-side and sell-side advice, helping clients capitalise on selective opportunities and position assets credibly to investors. With respect to aged assets, KR8 can help to find creative solutions and alternative investors to maximise investment value for the fund.

- Performance Improvement: our team of financial and operational experts can protect and drive value in the portfolio to make aged assets more saleable. We offer modelling support, cost reduction, working capital optimisation, operational restructuring and interim support.

- Portfolio restructuring: we assess viability, rationalise underperforming assets and implement restructuring strategies that stabilise portfolios and preserve value.

- Debt advisory services: we support refinancing, covenant negotiations and capital structure redesign to ensure businesses are appropriately leveraged in an increasingly volatile macro-environment.

Furthermore, our wider group has the capabilities to provide independent Due Diligence and Valuation, in response to conflicts brought about by continuation funds.

If you would like to discuss strategic options for your business or Portfolio Companies, please do get in touch.